MLC Retirement BoostTM

Unlock your clients' income potential.

What are you looking for?

ClientFirst: 1800 517 124

Unlock your clients' income potential.

Let's make sure they do so with confidence.

Download White PaperDelivering the potential for a higher income for life

At the heart of every retirement plan is the goal to help people retire with confidence and financial security.

That’s why we created MLC Retirement Boost - an innovative retirement income stream designed to increase the potential of your clients' super from their first contribution.

Contact usHow does MLC Retirement Boost work?

MLC Retirement Boost has two flexible phases:

MLC Retirement Boost (Super) functions like a standard superannuation account, while potentially enabling your clients to access means test concessions for the Government age pension.

The earlier your clients begin MLC Retirement Boost (Super), the greater their potential age pension entitlements.

MLC Retirement Boost (Pension) is designed to deliver retirement income for life, and can be used separately or alongside your clients’ account based pension.

MLC Retirement Boost gives your clients more options to access higher income in retirement!

MLC Retirement Boost is part of the growing category of innovative retirement income streams, helping Australians achieve a better retirement through:

Greater income flexibility than traditional annuities.

Confidence to spend more of their super.

Income for life, tailored to individual needs.

Let’s crack the egg

Exploring Retirement Boost features

Retirement Boost (Super) |

|||

|---|---|---|---|

Saving phase |

Accumulation account Receive contributions into this account as you would any superannuation account, subject to superannuation caps. You must withdraw, rollover or transition to Retirement Boost (Pension) when you meet a Specified Condition of Release. |

Full flexibility Funds can be withdrawn or transferred to another superannuation product without restrictions on capital. |

Age pension benefits You may accumulate Purchase Amount concessions, which could increase your Age Pension eligibility and entitlements when you transition into Retirement Boost (Pension). |

Retirement Boost (Pension) |

|||

Retirement phase |

Age pension benefits 60% on the Purchase Amount will be assessed under the asset test and 60% of income under the income test. |

Income for life Designed to provide you and your spouse (if the Spouse Option is selected) an income for life

|

Defer income and receive contributions You can choose to defer income in this account up until age 99. Whilst income is deferred, this account can accept contributions. |

|

Annual bonus To support the delivery of income for life, an Annual Bonus is credited to your account each year from the date you open or transition into a Retirement Boost (Pension). |

Death and Exit Benefit option You can choose a Death and Exit Benefit which may provide you and/or your beneficiaries with a benefit if you die or voluntarily exit. If you choose not to receive a Death and Exit Benefit, no benefit is payable on death or exit. |

Spouse option When you transition to or apply for a Retirement Boost (Pension) account, you may choose the Spouse Option. This allows you to nominate your spouse to continue to receiving income payments after your death. |

|

Retirement with a boost

Did you know? Retirement Boost can provide up to 60% more income in retirement when combined with the age pension*.

*Subject to individual circumstances and obtaining personal advice.

Creates more opportunities to demonstrate ongoing value of advice.

Simplifies holistic retirement income delivery through one platform.

Offers flexibility in strategy options to suit retirement goals.

Allows additional contributions during the deferral phase (e.g. inheritance, downsizer).

We’ve partnered with Challenger and TAL to provide support and help you consider MLC Retirement Boost for your clients. As part of this, we are developing a Centre of Excellence, giving you access to expert insights, practical tools, and dedicated support to elevate the value of your retirement advice.

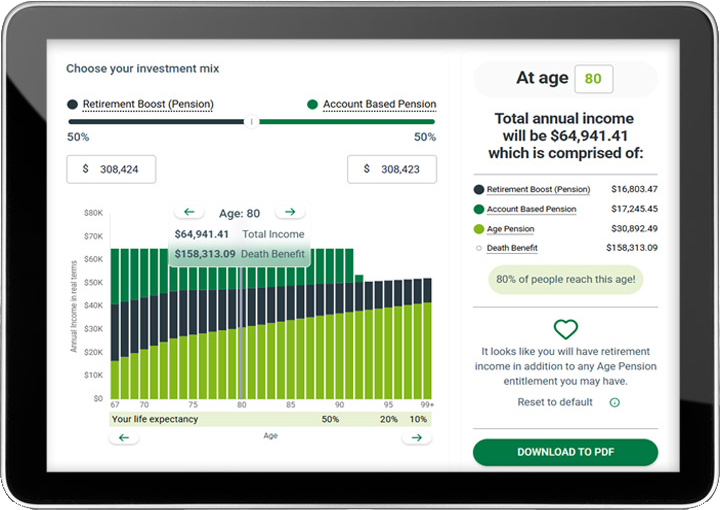

Discover the power of the Retirement Boost Optimiser

A powerful adviser tool designed to help you visualise your clients’ total retirement income across super, retirement and the age pension.

Log in to access the Retirement Boost Optimiser.

LoginImportant Documents

Can't find what you need?

Call us 8am–6pm Monday to Friday (AEST) on 1800 517 124.

Talk to us today

For more information, please contact your Business Development Manager, Relationship Training Manager or email.